By Anthony Raimondo

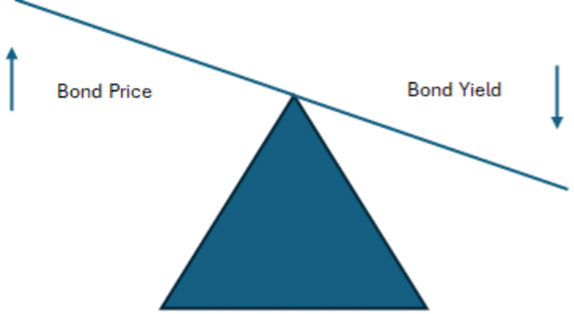

A core principle of fix-income investing is that bond prices move in the opposite direction of interest rates. To understand why this relationship exists, we first need to review what a bond is and the features that determine its price.

What is a bond?

A bond is simply a contract between a borrower (often a corporation or government) and a lender (investor or group of investors). The lender provides a lump sum to the borrower who promises to pay interest periodically (known as coupons) and return the investment at the end of the term.

By investing in a bond, you are assuming the position of the lender. You have the right to receive a series of future payments from the borrower.

What is a bond yield?

Think of a bond’s yield as the annual return (%) you could expect to earn each year if you buy the bond, reinvest its coupon payments, and interest rates stay about the same. It’s a way of answering, “What might I actually get back over time if things don’t change much?”

It can also be thought of as a single discount rate that makes the bond’s price match the value of all future payments it promises to make. It is the “balancing point” that connects what the bond costs now with what you’ll receive in the future. We use the term “discount rate” because you are discounting the value of the future payments owed to you based on the timeliness and likelihood of receiving the payments you expect.

You’re familiar with the time value of money. If a friend asked you to borrow $100 for one year, you’d want to receive, for example, $110 in return. You have set a discount rate (yield) of ![]() . Suppose your other friend, notoriously unreliable, asks for the same deal. You’d probably demand repayment of $115 instead (yield = 15%) or offer less than $100 upfront.

. Suppose your other friend, notoriously unreliable, asks for the same deal. You’d probably demand repayment of $115 instead (yield = 15%) or offer less than $100 upfront.

Interest Rates

All of this talk about bond yields… you’re probably wondering, “I thought we were covering bond prices and interest rates!”

Interest rates and bond yields are closely related, and the terms are often used interchangeably, but they are distinctly different.

Interest rates represent the cost of borrowing money. If you secured a mortgage in 2021, your interest rate may have been in the range of 2-3%. A few years later, that same loan had an interest rate of 6-7%. The cost of borrowing across the economy had shot up.

A bond’s yield, on the other hand, represents the borrowing cost for a specific borrower at the specific payment terms in the contract. It is determined by the price investors are willing to pay for the bond today, which is typically driven by supply and demand for the bond.

So why do bond yields typically mirror changes in interest rates?

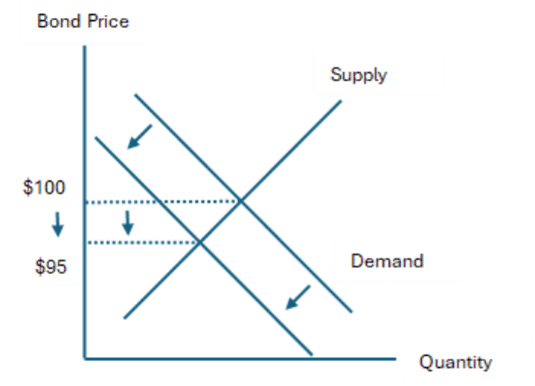

Imagine you own a bond with a 5% yield, meaning you could expect to earn an annual return of roughly 5%. If the economy-wide interest rate for the same borrowing term was 5%, you are likely content. But if that same interest rate increased to 6%, you are now missing out.

As you and many others sell your investment to go buy the new, higher-yielding bond, the price of your 5% yielding bond will fall until a willing buyer steps up to take it off your hands. They won’t be willing to pay as much as they would have yesterday, because their money could chase higher-yielding investments just like you are. Demand for your bond has fallen. Lower demand = lower price.

Remember what happens when a bond’s price falls? The yield goes up!

Conversely, a lowering of interest rates to 4% now makes your 5% yielding investment more attractive. More investors now want to own the same bond as you, and the increase in demand lifts the price of the bond and lowers the yield.

Bottom line: when interest rates change, the opportunities in the bond market change and supply and demand dynamics find a new equilibrium for each bond. The payment schedule of bonds across the market does not change, but prices must adjust, and bond yields are there to balance the two sides of the equation.

What affects interest rates?

There is no single model or equation that can explain where interest rates should be or where they are headed. They are influenced by a combination of policy decisions, economic conditions, and supply and demand forces.

Keep in mind, short-term interest rates – think one year or less – are likely different than long-term rates of 10+ years. Each provides insight into different parts of the economy, and they are influenced by different factors.

In most countries, central banks set benchmark interest rate targets based on economic conditions. This is known as Monetary Policy. To fight off recession, interest rates can be lowered to reduce the cost of borrowing and encourage economic activity. The exact opposite action can be taken to fight inflation or prevent the economy from overheating. These actions directly affect short-term interest rates.

The federal government can also stimulate the economy by increasing spending and lowering taxes, which is known as Fiscal Policy. These actions often require governments to borrow more, which damages the confidence investors have in the government’s long-term financial stability. In this example, prices for long-term government bonds will fall in this case, because, among other factors, investors are not as certain the government will be able to pay them back. You know what this means… Price ↓ Yield ↑

Naturally occurring forces also affect interest rates directly and inform the policy decisions we just covered. For example, if inflation is high or expected to rise, lenders may increase the interest rate they charge to protect the purchasing power of the future payments they are owed. If businesses are growing and consumers are spending, they may be more likely to borrow money to support their activities. Remember, interest rates represent the cost of borrowing money: higher borrowing demand = higher cost of borrowing.

What else affects a bond’s price?

Although the prices of all bonds are affected by the changing interest rate environment, some are impacted more than others. The sensitivity of a bond’s price relative to interest rate changes is most heavily influenced by the length of the loan. If you expected interest rates to increase, you’d be reluctant to lock up your money today for ten years, but you might consider doing so for six months. The price of the long-term bond will fall by more than a shorter-term alternative.

For a specific borrower, their creditworthiness will affect their borrowing rate. Remember your two loan-seeking friends from earlier? Your unreliable friend was more of a credit risk from your perspective. You would demand a higher yield to be compensated for the increased risk of lending them your money.

A variety of other factors also affect the price of a bond, such as how easy or difficult it is to find another investor to sell to (liquidity), or unique features of the payment terms – like the ability to repay the loan early. But most importantly, you should remember that interest rates establish a benchmark for borrowing rates, and borrower-specific factors determine the credit risk of a given bond.