History likely will not repeat itself, but it may rhyme.

Tune in as Chief Investment Officer at Blue Chip Partners, Daniel Dusina, CFA, and Managing Partner, Dan Seder, CFA, CMT, CFP® discuss the historical precedent for recent strength in the stock market, as well as why Dusina thinks bonds currently present a “once in a decade” investment opportunity.

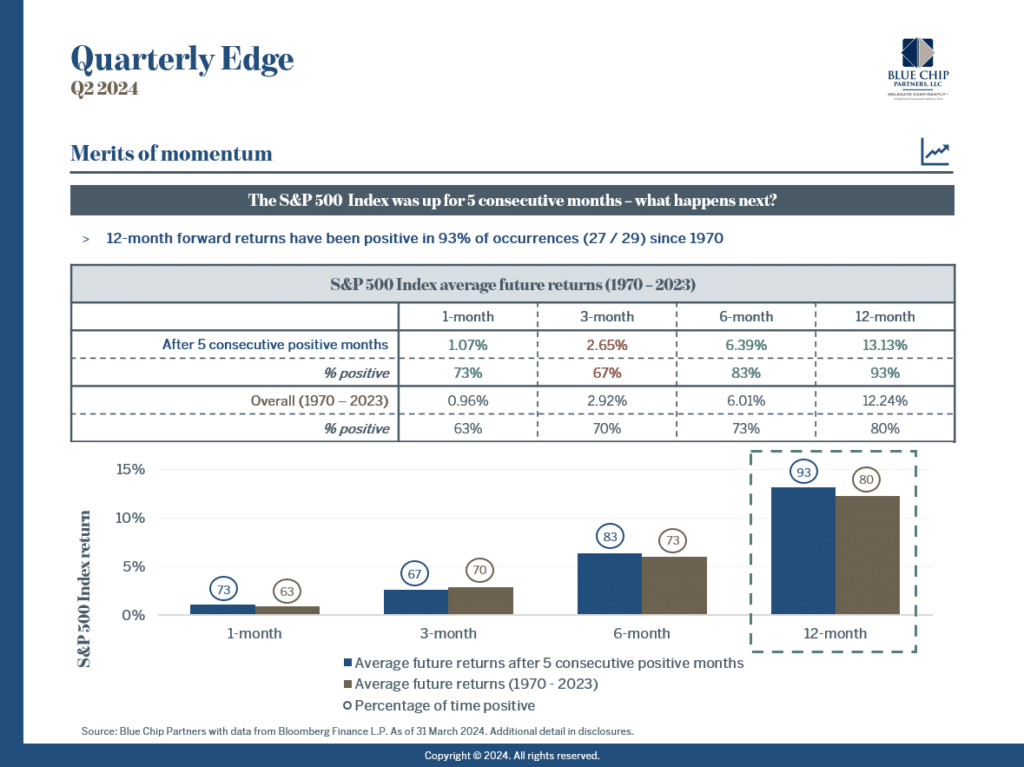

Data points to upward momentum in stocks continuing for another 12 months after 5 straight months of growth.

In this clip from our recent podcast episode, Blue Chip Partners Chief Investment Officer Daniel Dusina, CFA shares what recent strength in the stock market could indicate for the path forward, as well as why Q1 2024 portrayed a healthier equity market than the same period last year.

Should I move my money market funds to bonds? Data shows insights into why now may be the time.

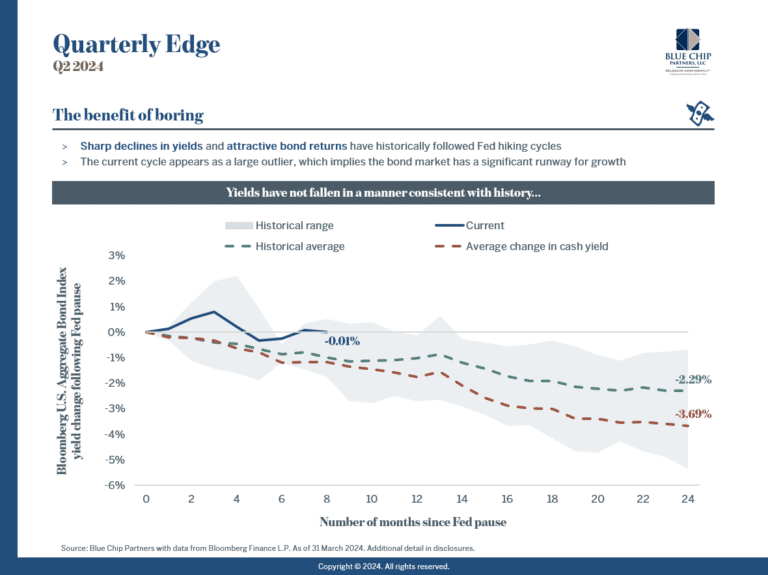

It has not been uncommon historically for bond yields to fall, bond prices to rise, and cash yields to drop after the final hike in a Federal Reserve cycle. This time, the opposite has happened.

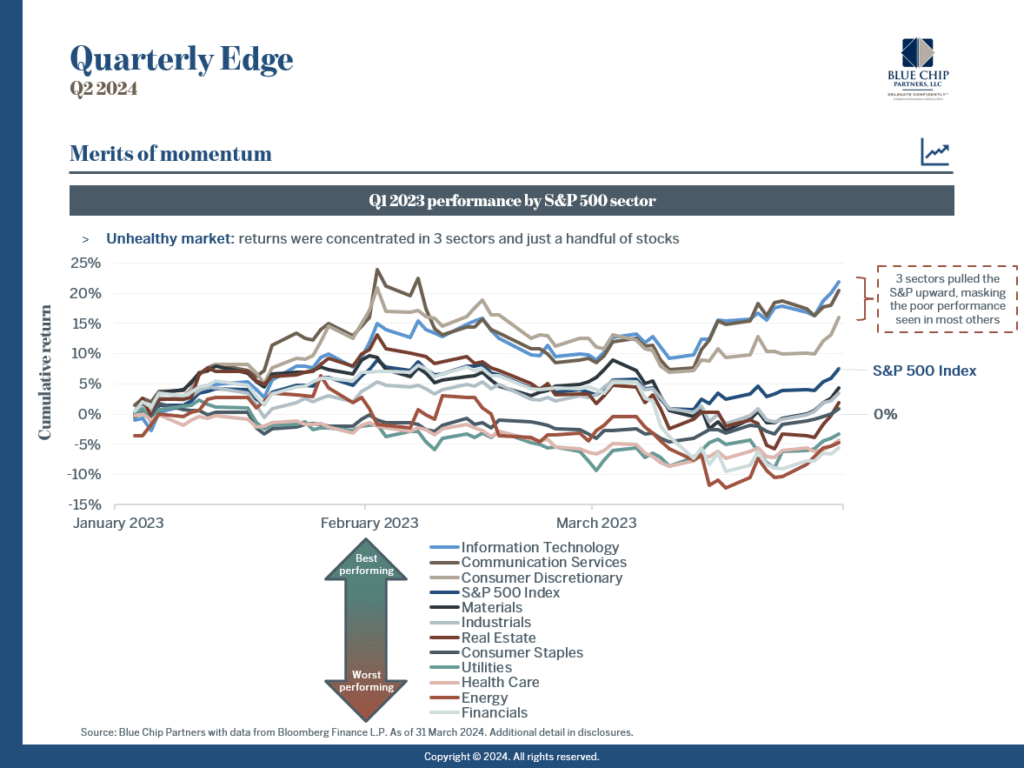

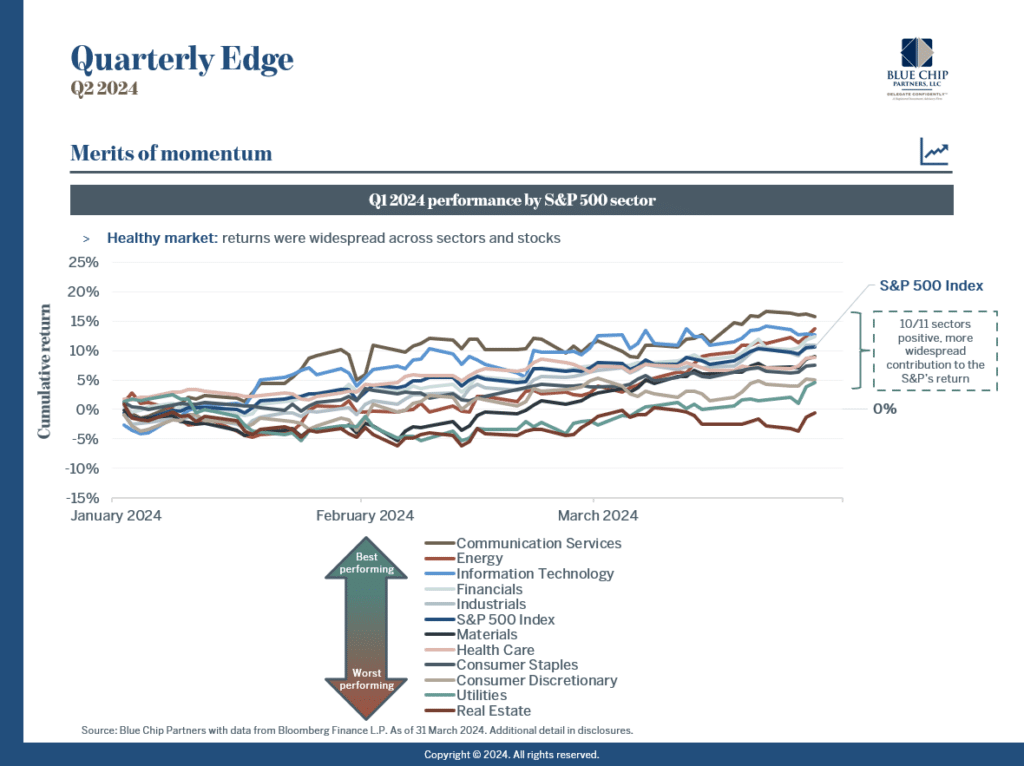

In the first quarter, U.S. stocks as measured by the S&P 500 Index gained 10.55%. Seemingly picking up where 2023 left off, the U.S. market has returned ~26% over the previous 5 months – all of which displayed upward movement in the index. After a period of meaningful appreciation in the domestic equity market, it is common for investors to question the potential for further gains in the immediate term. While we are not in the business of predicting short-term price movements, we are encouraged by the healthy fundamentals across the corporate landscape. These include continued growth in both revenue and earnings as well as greater balance in the labor market. Further, performance of the U.S. equity market has been much more widespread in 2024 relative to 2023 (a component of our optimistic stance in the Q1 Quarterly Edge), which we would view as reflective of a healthy market.

Finally, while we do not expect history to repeat itself, it certainly may rhyme with what is to come. Historical data indicates that 5 consecutive months of upward movement in the S&P 500 does not necessitate a pullback. In fact, future returns from the index have historically been higher than the long-term average after 5 consecutive months of positive performance, and have been more frequently positive over periods following a 5-month winning streak (full details found below). While we would not be surprised to experience periods of greater choppiness given lack thereof in recent months, both historical data and underlying fundamentals leave us optimistic on the trajectory of U.S. stocks.

The Benefit Of Boring

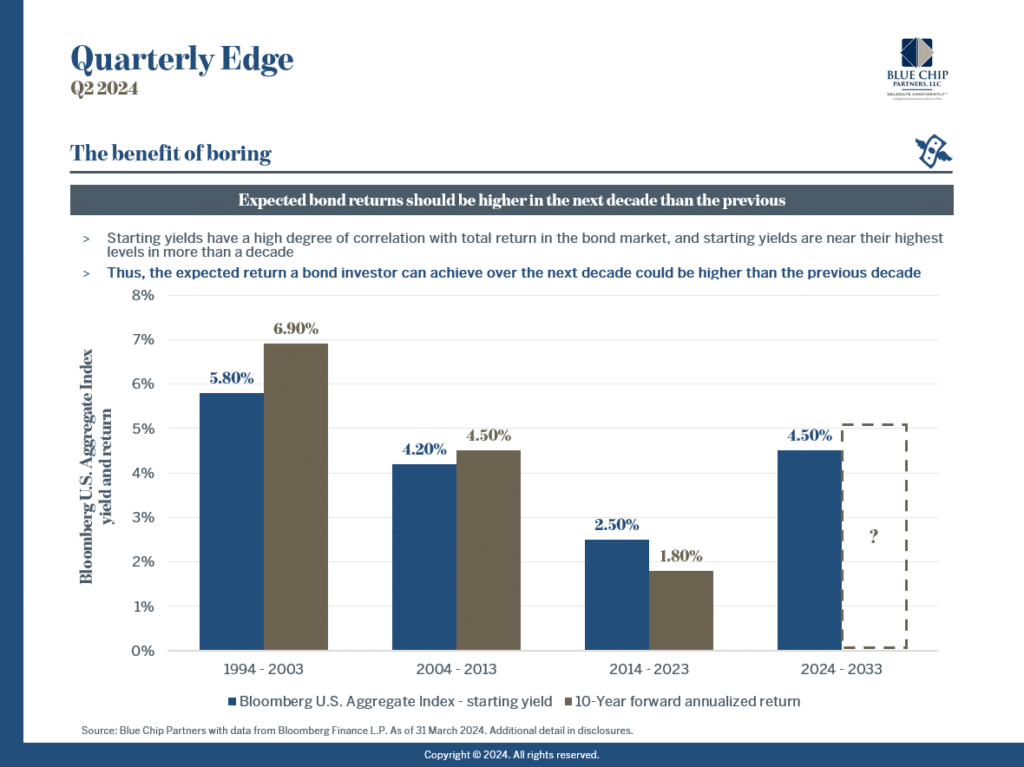

For the better part of the last year, we have been vocal with regards to why we view the bond market as ripe for investment. Now more than ever, our constructive thesis holds. Our optimism can be distilled into two primary points:

- Starting yields are near their highest levels in more than a decade, and

- The Federal Reserve is expected to start reducing interest rates this year

On the first point, it is imperative to understand that the initial yield of an investment in the bond market has historically been the best predictor of total return. If an investor purchases a 10-year Treasury bond at par yielding 4.00%, when held to maturity, the return experienced will be 4.00%. Prices can fluctuate in the secondary market based on interest rate movements throughout the life of a bond (bond prices and interest rates are inversely correlated), but income will be the primary driver of return – especially when the level of income generated is more sizable.

In 2023, for example, higher starting yields played a pivotal role in driving return. The 10-year Treasury touched 5% in October, and despite meaningful interest rate volatility throughout the year, the 10-year yield ended the year precisely where it began – 3.88%. Even though rates moved higher through October, returns in most subsets of the fixed income market remained positive or only modestly dipped into negative territory as income distributions served to offset price declines. 2022 was a different story, as meaningfully lower starting yields were unable to buffer against hefty upward movements in interest rates. In fact, the combination of low starting yields and severe price declines had a significant negative impact on a decades’ worth of return, as you can see in the chart that follows. Thus, with starting yields close to multidecade highs, today’s bond market should be viewed as compelling.

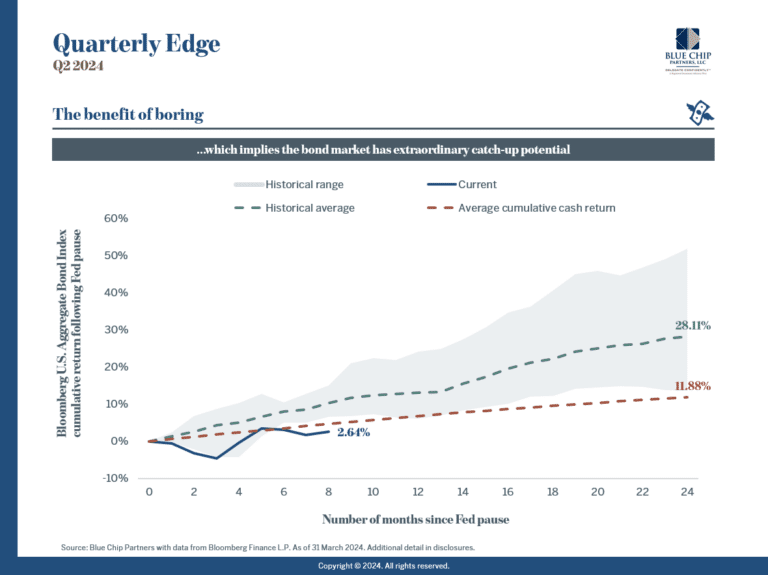

Though income drives the bulk of bond returns, price movement remains a factor as well, and history suggests that today’s bond market is still in the early going of a lengthier rally. Persistent upward movement in the fixed income market has been visible following the end of Fed rate hiking cycles using data since 1978, while cash returns falter given the rate cuts that follow soon after. Today’s yields have only fallen by a fraction of the average historical decline, and returns since the end of the Fed’s hiking cycle (July) have not kept pace with what has previously been observed. This reinforces our stance that the time to begin a shift away from cash assets and towards bonds is now.

Sharp declines in yields and attractive bond returns have historically followed Fed hiking cycles. The current cycle appears as a large outlier, which implies the bond market has a significant runway for growth

Disclosures:

Expressions of opinion are as of 31 March 2024 and are subject to change without notice. Any information provided is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation to buy, hold, or sell any security. There are limitations associated with the use of any method of securities analysis. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Every investor’s situation is unique, and you should consider your investment goals, risk tolerance, and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Past performance does not guarantee future results. Investing involves risk, and you may incur a profit or loss regardless of strategy selected. There is no guarantee that any statements, opinions, or forecasts provided herein will prove to be correct. Dividends are not guaranteed and must be approved by the company Board of Directors. Indices are included for informational purposes only; investors cannot invest directly in any index.

S&P 500 Index average future returns (1970 – 2023): Source: Bloomberg Finance L.P. Returns are shown for the S&P 500 Index from 31 January 1970 – 31 December 2023. The S&P 500 Index is a market capitalization weighted index that tracks the performance of 500 of the largest companies that are listed on stock exchanges in the United States. It is not possible to invest directly in an index.

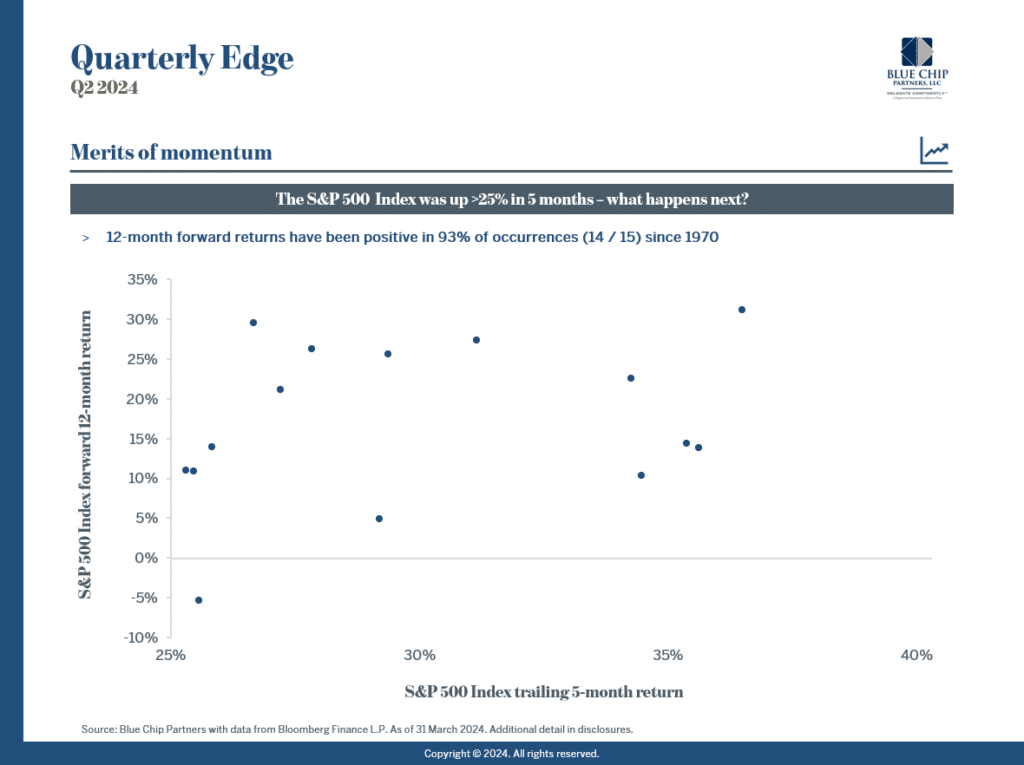

S&P 500 Index average 12-month returns (1970 – 2023): Source: Bloomberg Finance L.P. Returns are shown for the S&P 500 Index from 31 January 1970 – 31 December 2023. Data included is representative of periods in which the index returned a value greater than 25% over a 5-month period. The S&P 500 Index is a market capitalization weighted index that tracks the performance of 500 of the largest companies that are listed on stock exchanges in the United States. It is not possible to invest directly in an index.

Q1 2023 / Q1 2024 performance by S&P 500 sector: Source: Bloomberg Finance L.P. Returns are shown for the various sector indices that underlie the S&P 500 Index from 31 December 2022 – 31 March 2023. The S&P 500 Index is a market capitalization weighted index that tracks the performance of 500 of the largest companies that are listed on stock exchanges in the United States. It is not possible to invest directly in an index.

Expected bond returns should be higher in the next decade than the previous: Source: Bloomberg Finance L.P. Yields are representative of yield to worst. Returns and yields are shown for the Bloomberg U.S. Aggregate Bond Index, and are representative of the 10-year periods between 31 December 1993 – 31 December 2023. The Bloomberg U.S. Aggregate Index is a broad-based fixed income benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. It is not possible to invest directly in an index.

Yields have not fallen in a manner consistent with history…which implies the bond market has extraordinary catch-up potential: Source: Bloomberg Finance L.P. Yields are representative of the yield to worst for the Bloomberg U.S. Aggregate Bond Index and the current yield of the U.S. Generic Government 3-Month Index. Returns and yields for the two aforementioned indices are calculated from the end of the month in which the Federal Reserve stopped raising rates in 1981, 1984, 1989, 1995, 2000, 2006, and 2018. The Bloomberg U.S. Aggregate Index is a broad-based fixed income benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The U.S. Generic Government 3-Month Index is a fixed income benchmark that tracks 3-month Treasury bills offered by the U.S. government. It is not possible to invest directly in an index.