The Resilient U.S. Economy: Growth, Inflation, and Market Shifts

The U.S. economy continues to show resilience, even as the landscape grows more complex. In this edition of our Quarterly Edge, we take a close look at the forces that appear to be shaping markets today: strong consumer spending, signs of labor market softening, inflation risks, and the potential for money in motion as the Federal Reserve cuts rates.

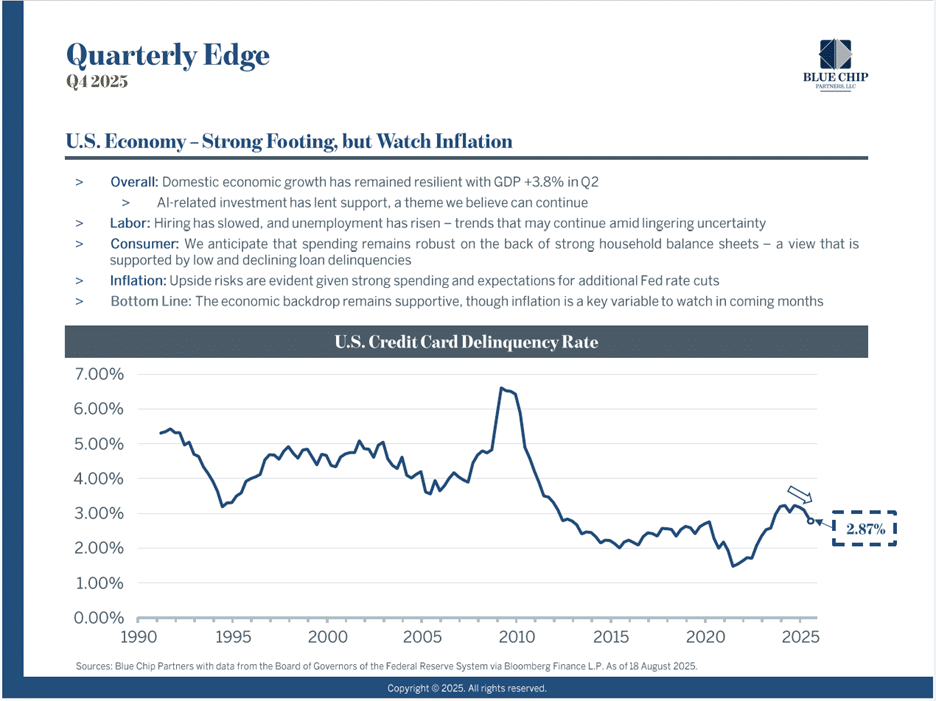

GDP growth was revised up to 3.8%, supported in part by AI-driven business investment. Consumers remain the backbone of the economy, with robust balance sheets and declining credit card delinquencies signaling financial health. At the same time, unemployment has ticked higher and job creation is slowing, which highlights why the Fed has shifted toward easing rates to support employment.

Inflation remains the balancing act. While it has moderated overall, risks of a rebound are evident given resilient spending and easier financial conditions. As we’ve stressed, if policymakers ease too much, we run the risk of reigniting inflation.

Market Valuations and Opportunities

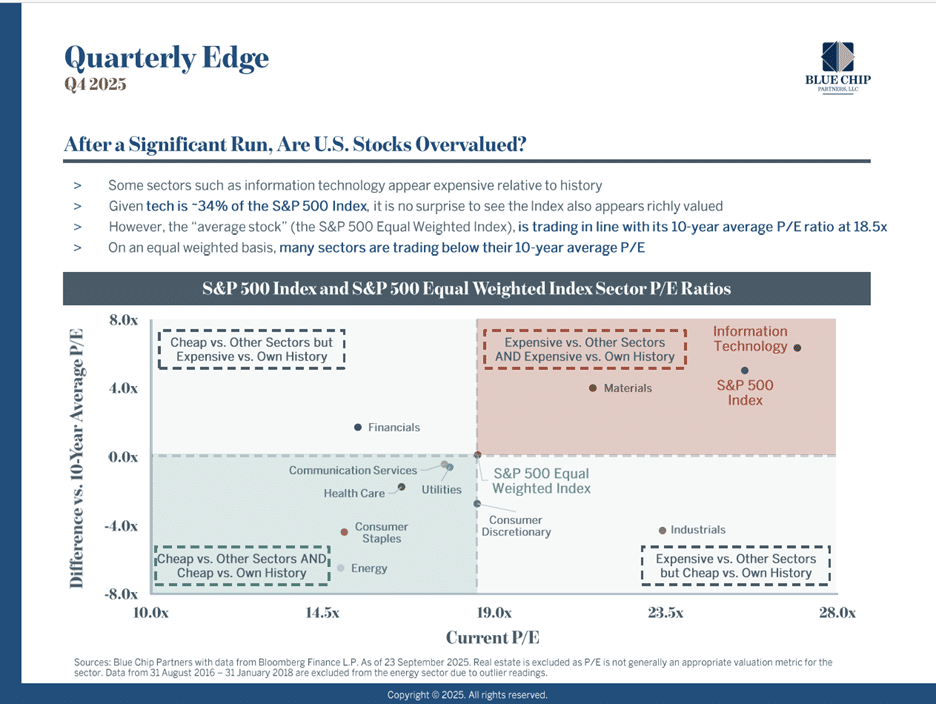

After a significant run in equities, concerns about valuations are front of mind. The S&P 500 Index, heavily weighted toward large-cap tech, appears richly valued. Yet the “average stock” — as represented by the equal-weighted S&P 500 — is trading right at its 10-year average P/E of 18.5x. Several sectors, including consumer discretionary and healthcare, appear undervalued both versus history and peers.

This underscores why we believe selectivity matters most. Rather than relying on broad index exposure, investors should focus on identifying high-quality businesses trading at more attractive valuations.

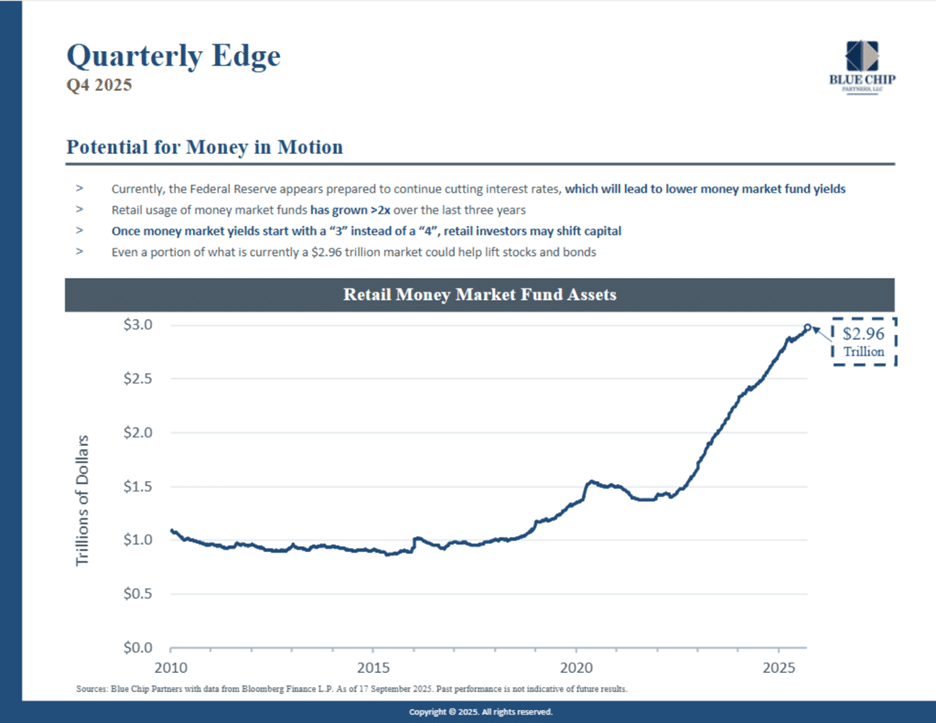

The Coming Shift: Money in Motion

One of the most important dynamics to watch in the months ahead is the shift in money market fund allocations. With retail money market assets now at $2.96 trillion (as of September 2025), investor psychology will play a critical role.

As Fed cuts drive yields lower, we believe the behavioral tipping point will come once money market yields start with a “3” instead of a “4.” At that point, many investors will likely begin reallocating cash toward stocks and bonds — a move that could provide meaningful fuel for markets in the coming year.

Key Takeaways

- Economic Growth: U.S. GDP revised to +3.8%, highlighting resilience despite labor softness.

- Consumers Strong: Household balance sheets remain solid; delinquencies are declining.

- Inflation Watch: Upside risks remain as the Fed prioritizes labor support.

- Market Valuations: Large-cap tech is expensive, but many sectors trade below their historical averages.

- Money in Motion: Lower money market yields could spark capital shifts into risk assets.

Final Thoughts

The U.S. economy stands on strong footing, but investors should remain alert to inflation, labor market shifts, and the psychology driving consumer and investor behavior.