Liberation Day to Bond Stability: Navigating Uncertainty

As we entered the second half of 2025, unresolved trade tariffs, shifting labor dynamics, and heightened geopolitical tensions weighed heavily on investor sentiment. In this edition of our Quarterly Edge, we explore how these forces are reshaping both markets and investor psychology.

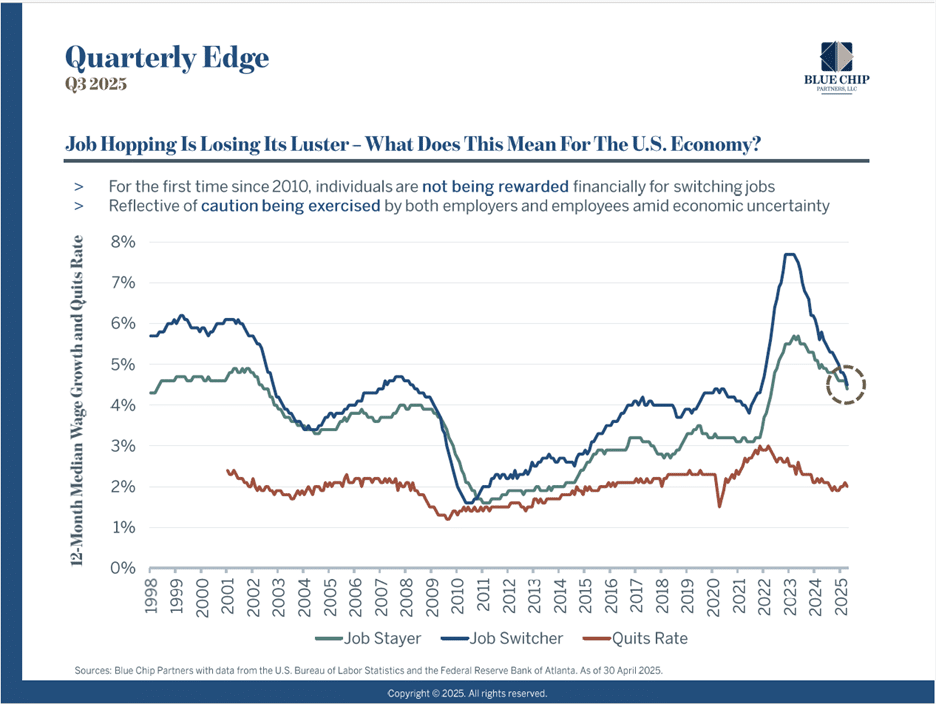

One emerging theme: labor market behavior is changing. For the first time in over a decade, job-switchers are no longer receiving significantly higher wage increases compared to workers staying put. This shift reflects growing corporate caution as businesses prepare for potential policy and economic headwinds. As we put it on the episode: “Job-switchers are no longer financially incentivized like they were for the past 15 years—and it shows in the data.”

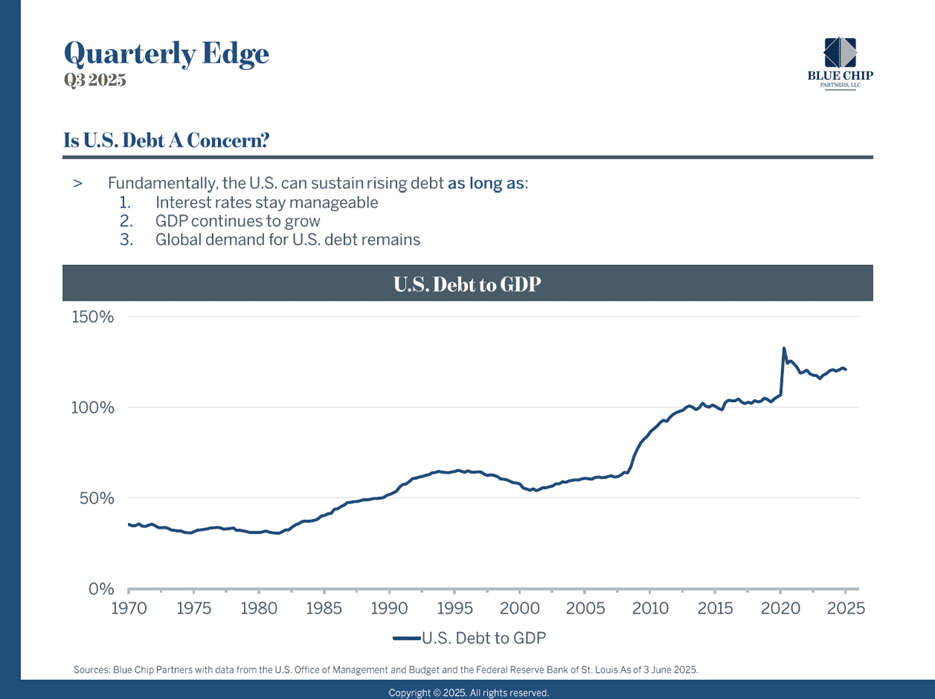

At the same time, U.S. debt levels are drawing more attention. The concern is less about the sheer math of rising debt-to-GDP ratios and more about perception: markets often move on confidence as much as fundamentals. “Debt levels themselves don’t cause market disruption—perception does.”

Market Reactions: From Liberation Day to Geopolitical Tensions

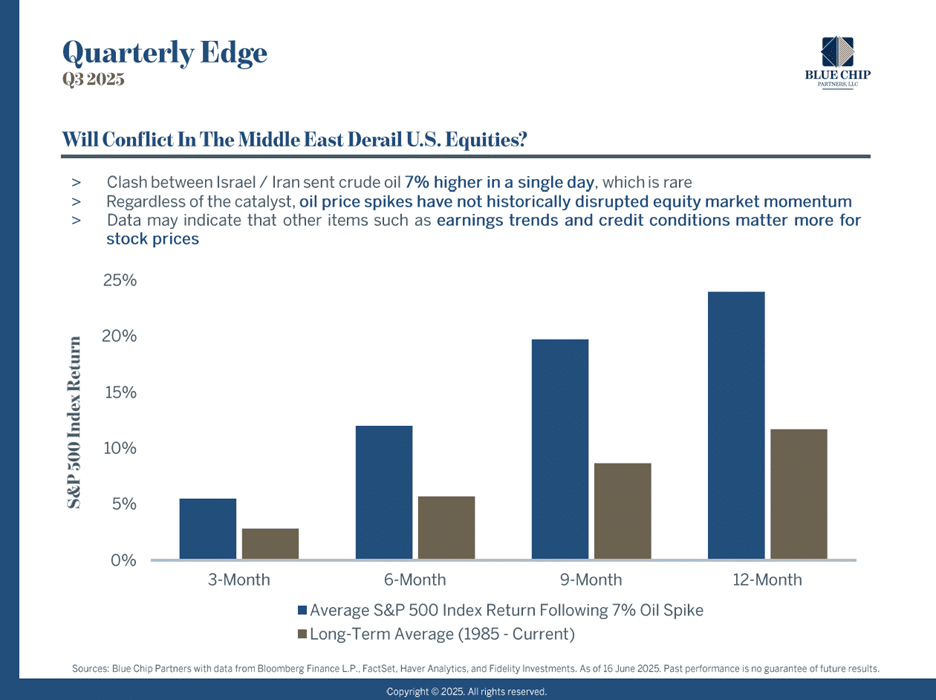

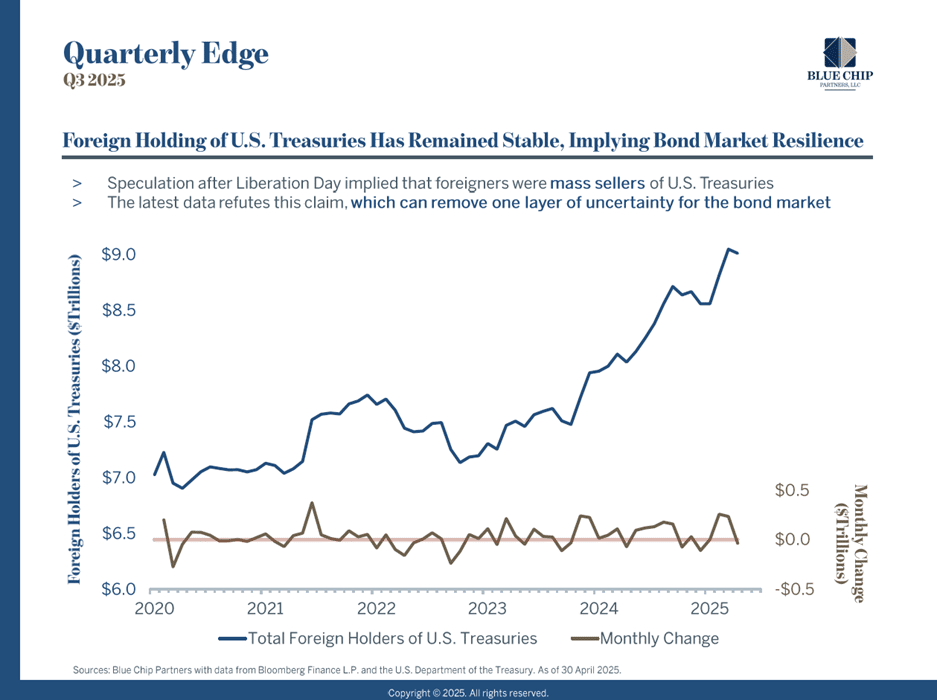

We also reflected on the post-Liberation Day sell-off, when markets reacted sharply to tariff headlines and renewed global uncertainty. Sector-specific volatility has persisted, with heightened sensitivity to international developments, including the ongoing Israel-Iran conflict.

Despite these headwinds, the bond market has stood resilient. Higher yields have made fixed income allocations increasingly attractive, while strong foreign demand continues to support stability. As we emphasized: “Foreign demand for U.S. debt is the linchpin—if it breaks, so does the narrative of stability.”

Key Takeaways

- Tariff Uncertainty: Potential policy changes are weighing on corporate behavior and investor confidence.

- Labor Shifts: Wage growth for job-switchers has flattened, signaling caution from employers.

- Debt Perception: Rising U.S. debt-to-GDP is as much a matter of market psychology as fiscal arithmetic

- Geopolitics & Markets: Liberation Day volatility and regional conflicts underscore persistent fragility

- Bond Market Strength: Higher yields and sustained foreign demand point to resilience in fixed income.\

Watch the Full Discussion

🎥 Watch Quarterly Edge – Q3 2025 on YouTube